When you hear Richard Nixon, you think of Watergate. The 37th President of the USA remained in the world’s minds as a power-obsessed cynic who wanted to bug the Democratic Party headquarters in the Watergate complex and who was forced to resign on August 9, 1974 after an unprecedented impeachment. But Nixon was also a president who changed the world. He established diplomatic relations with the People’s Republic of China, but above all blew up the post-war monetary system.

Fifty years ago, on August 15, 1971, in a radio and television address, Nixon unilaterally renounced the United States’ obligation to exchange dollars for gold. The dollar lost its function as an anchor for the other currencies overnight. The rest of the world was completely unprepared for the speech, which is why it went down in history as the Nixon shock. The shock changed the way people think about the market and the state around the world. In Europe it triggered a dynamic that decades later would lead to monetary union and the euro.

The currency system that had been in effect until then had been decided by the later victorious powers of World War II at a conference that met from July 1 to 22, 1944 in the resort of Bretton Woods in the US state of New Hampshire. The main participants were the head of the American delegation, Harry Dexter White (he would later be exposed as a Soviet spy), and the British economist John Maynard Keynes. Both came to Bretton Woods with different concepts, with White prevailing – unsurprisingly given the economic strength of the USA.

White’s plan was that all currencies would be pegged to the dollar at a fixed rate. To compensate for this, the US committed itself to exchanging its currency for gold at any time at a price of $ 35 per troy ounce. For comparison: On Friday afternoon, gold costs around $ 1,770. An International Monetary Fund (IMF) should help countries with payment difficulties.

The Bretton Woods system initially proved incredibly successful after the war. The economy of the western world grew at a rate that was unprecedented in historical terms. World trade flourished, inflation remained under control, and unemployment fell. In the 1960s, many believed that the “golden age of capitalism” had begun, as historian Harold James wrote.

Bretton Woods made the young Federal Republic an export nation for the economic miracle

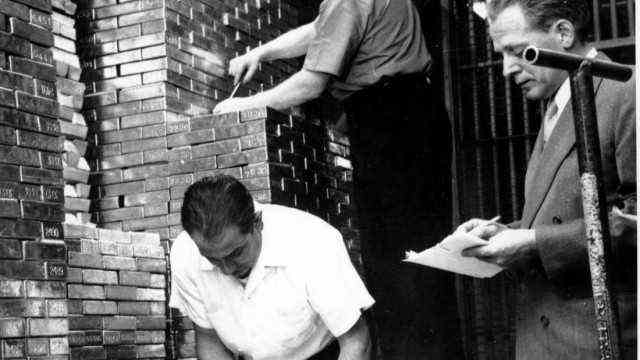

The young Federal Republic of Germany particularly benefited from Bretton Woods. Their economic miracle was thanks to the Minister of Economics, Ludwig Erhard, but also to the Bretton Woods system. The stable exchange rates made it possible for the Federal Republic of Germany to become an export power, although it certainly helped that the D-Mark was at times grossly undervalued. Because the Germans exported much more than they imported, they were able to build up huge gold reserves under Bretton Woods. Even today, Germany has the second largest gold reserves in the world after the United States. The gold bars weigh a total of around 3400 tons and are stored in the vaults of the Bundesbank in Frankfurt, the Federal Reserve Bank of New York and the Bank of England.

Gold bars in the US Federal Reserve, the recording dates from 1962.

(Photo: AP)

For all its successes, however, the system had a weaving flaw: a growing world economy needed more dollars. These additional dollars were backed less and less by gold, and America’s current account was in deficit. This had to lead to a crisis of confidence at some point. The problem was discovered early on by the Belgian economist Robert Triffin, which is why it is still called the Triffin Dilemma today. In the late 1960s it became apparent how right Triffin was. Speculators attacked the dollar more and more aggressively and instead relied on the D-Mark. That couldn’t go on for a long time.

At least that was what a largely unknown economist in the US Treasury Department was convinced of. His name was Paul Volcker and would later become famous as head of the Federal Reserve (1979 to 1987) and advisor to President Barack Obama during the financial crisis (2009). At the beginning of 1969, however, he had just moved from a bank to the ministry as State Secretary for Currency Crises. Volcker was actually close to the Democrats, but he joined the government after Republican Nixon took office because he saw an opportunity to fight currency devaluation in the United States. Inflation had now passed the five percent mark – not too much for what was to come in the seventies, but worrying at the end of the so far so successful sixties.

On behalf of Treasury Secretary John Connally – like Volcker a Democrat – he developed a concept that was supposed to limit inflation and restore confidence. Nixon and Connally agreed to the concept. It was then discussed and decided in strict secrecy at the country residence of the American President in Camp David. The conference began on the evening of August 13, 1971, a Friday, and ended the following Sunday morning. When Nixon announced the results on radio and television that evening, 46 million Americans watched or listened.

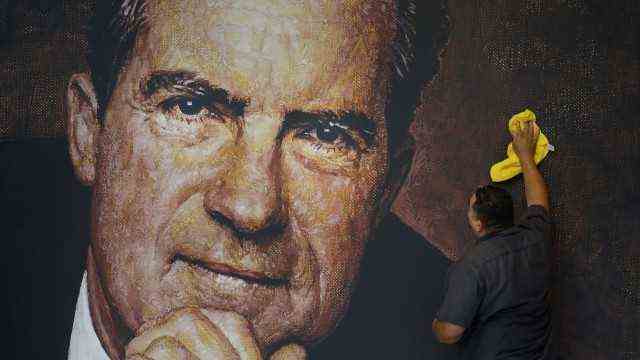

His speeches are documented in Nixon’s presidential library. He sold the proclamation of the gold standard as a great liberation.

(Photo: Jae C. Hong / AP)

Nixon’s program consisted of three parts. First, the US unilaterally untied the dollar’s peg to gold. Second, the government issued a general price freeze for 90 days. And third, it imposed an import tariff of ten percent to compensate for allegedly unfair exchange rates. The response to the speech in America has been consistently positive. When the New York Stock Exchange opened on Monday, Chrysler’s shares were up 15 percent, those of Ford and General Motors up 10 percent each.

The situation was a little different for American tourists abroad. They got to feel how little esteem their currency still had. Taxi drivers in Paris charged a surcharge if they were to accept dollars as a means of payment. A couple complained Wall Street Journal in Rome, they couldn’t even have bought an ice cream cone with their dollars. Even German tourists in other European countries who had taken dollar travelers’ checks with them to be on the safe side had to worry about their money for a few days.

Rhetorically, however, Nixon’s speech was brilliant. He sold the emergency measures as a major blow: “The time has come for a new economic policy in the United States,” he said. “We have to create more and better jobs. We have to stop the rise in the cost of living, we have to protect the dollar from the attacks of international money speculators.” That was well received by the voters. Nobody asked why the government and central bank didn’t do the next best thing to protect the dollar: raise interest rates and cut government spending. The answer would have been awkward, as it would have sparked a recession and put Nixon’s re-election at risk.

Indeed, the Nixon shock was a failure. After the 90-day price freeze, prices rose, as expected, all the faster. The import tax hardly helped the domestic industry, and the dollar crises did not stop either. In December 1971 the industrialized countries agreed again on a reformed exchange rate system. The dollar was devalued and the fluctuations in exchange rates increased. But this Smithsonian Agreement, named after the building in Washington in which it was decided, only lasted a year. In early 1973, speculation against the dollar started again. On March 1, the Deutsche Bundesbank had to borrow no less than $ 1.7 billion to support the currency’s rate. Then it came to a “showdown” like that Bundesbank magazine in retrospect writes: The Vice President of the Bundesbank, Otmar Emminger, traveled to a cabinet meeting in Bonn to ask Federal Chancellor Willy Brandt to stop supporting the dollar. A day later, Brandt agreed, whereupon the Bundesbank stopped buying. That was the definitive end of Bretton Woods and the beginning of a new era.

The exchange rates of large currencies such as the dollar, D-Mark, Franc or Yen were no longer politically fixed, but were formed freely on the foreign exchange markets. The concept of flexible exchange rates originally came from the economist Milton Friedman, who taught at the University of Chicago. Friedman and the monetarists close to him wanted the state to stay out of the way, not only from the currency markets, but also from economic management in general. Instead, the central banks should only ensure that the money supply grew in a controlled manner so that prices remained stable. Friedman was awarded the Nobel Prize in Economics in 1976. In 1973, the Bundesbank was the first central bank to adopt Friedman’s ideas and adopt a monetarist concept of money supply. Since she no longer had to prop up the dollar, she could devote herself entirely to fighting inflation. This increased the power and prestige of the Frankfurt central bankers.

The Nixon shock had another long-term consequence in Europe: the Europeans united to fix exchange rates among themselves. That began in 1972 with the so-called currency snake, in which the members of the European Economic Community (EEC), Great Britain, Switzerland and a few others took part. The snake was followed in 1979 by the European economic system, which was supposed to create a unified economic area on the continent. The culmination of this development was the euro in 1998.